|

|

|

|

January 15, 2008

the great subprime majority

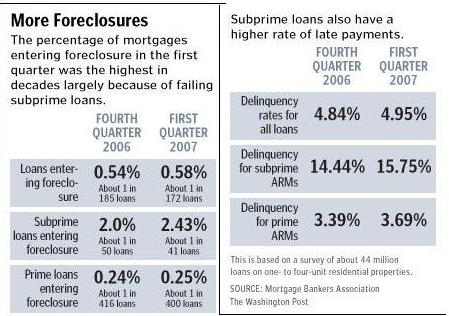

Pat Buchanan thinks things are bad. Basically, the economy is ruined, and we are hopelessly in debt, on the verge of economic collapse, and there is no hope: With the dollar sinking, oil surging to $100 a barrel, the Dow having its worst January in memory, foreclosures mounting, credit card debt going rotten, and consumers and businesses unable or unwilling to borrow, we appear headed into recession.Sounds like Hillary Clinton, except instead of offering socialism while denying it's socialism, Buchanan thinks the enemy is globalism, and how dare anyone call him an isolationist! We borrow from the nations we defend so that we may continue to defend them. To question this is an unpardonable heresy called "isolationism."Not if we can work together and throw enough rocks through corporate windows in Seattle! It's all the fault of a self-indulgent generation which is hopelessly in debt: This self-indulgent generation has borrowed itself into unpayable debt. Now the folks from whom we borrowed to buy all that oil and all those cars, electronics and clothes are coming to buy the country we inherited. We are prodigal sons, and the day of reckoning approaches.We? An entire generation has borrowed itself into unpayable debt? Well, the piece is called "Subprime Nation," so apparently that's his argument. Let's start with the definition of subprime mortage: A subprime mortgage, is a type of loan that is offered at a rate above prime to individuals who do not qualify for prime rate loans due to less-than-perfect credit history. Lenders charge a higher interest rate to compensate for potential losses from customers who may run into trouble or default.OK, so for starters, the loans which are especially plagued by the high foreclosure rates were not made to an entire generation, but to people with bad credit. There is no denying that foreclosures are at record highs. But I wonder how many of the people who read Buchanan's condemnation of an entire generation know the actual percentages of foreclosures. This has become such a political football that it might surprise people to know that most homes are not in fact facing foreclosure. Far from it. According to the Mortgage Bankers Association, the new foreclosure rate is slightly over a half of one percent: New foreclosures for prime and subprime borrowers combined hit record highs. They rose to 0.58 percent on a seasonally adjusted basis, compared with 0.54 percent in the previous quarter and 0.41 percent a year earlier.An accompanying chart illustrates:

USA Today looked at the total percentage of loans in foreclosure: The percentage of loans in the foreclosure process rose to 1.69% of loans outstanding, up 0.29 percentage point from the prior quarter and up 0.64 from a year earlier.Don't read me wrong. I am not denying the seriousness of the problem. An increase in the foreclosure rate is bad, and I think it was highly irresponsible to make the subprime loans that have turned out to be the worst offenders. Clearly, there were a lot of irresponsible loans made to irresponsible people. I'd even go along with Buchanan that such people are self-indulgent as he claims. But since when does a self-indulgent 2% become a generation? Don't the other 98% count? Sigh. (I guess I should be glad Buchanan didn't apply his communitarian math to human sexuality, or he'd say we've all become subprime homos.) posted by Eric on 01.15.08 at 07:53 PM

Comments

So all that Nixon administration price control, stagflation stuff was better? Since he was part of it? John Lynch · January 16, 2008 01:58 AM Buchanan underrates the ability of self-interested individuals to correct their courses, which is of course the germ of social and national correction as well. That having been said, this, too, must be: we've borrowed an awful lot of money, both individually and nationally. It really does have to stop. But these past hundred years, telling politicians to stop borrowing has had all the practical effect of research on male breast-feeding. Which receives federal funding, by the way. Francis W. Porretto · January 16, 2008 04:49 AM If you dig down into the record - what we've got with .58% is pretty low. How about 2.47% in 1997, or 1.21 in 1966? See Appendix, Table A in http://www.fdic.gov/bank/analytical/working/98-2.pdf Unless I misread this, which is a possibility, we ain't anywhere CLOSE to the highs of the last 50 years. Of course, with a 24/7 news cycle, EVERYTHING has to be the WORST PROBLEM EVER, or it won't get any attention at all. But a bit of historical perspective might be appropriate. (Oh, wait - historical perspective from the media? I'm dreaming. Let me go get some coffee and wake up!) JLawson · January 16, 2008 07:20 AM Post a comment

You may use basic HTML for formatting.

|

|

January 2008

WORLD-WIDE CALENDAR

Search the Site

E-mail

Classics To Go

Archives

January 2008

December 2007 November 2007 October 2007 September 2007 August 2007 July 2007 June 2007 May 2007 April 2007 March 2007 February 2007 January 2007 December 2006 November 2006 October 2006 September 2006 August 2006 July 2006 June 2006 May 2006 April 2006 March 2006 February 2006 January 2006 December 2005 November 2005 October 2005 September 2005 August 2005 July 2005 June 2005 May 2005 April 2005 March 2005 February 2005 January 2005 December 2004 November 2004 October 2004 September 2004 August 2004 July 2004 June 2004 May 2004 April 2004 March 2004 February 2004 January 2004 December 2003 November 2003 October 2003 September 2003 August 2003 July 2003 June 2003 May 2003 May 2002 AB 1634 MBAPBSALLAMERICANGOP See more archives here Old (Blogspot) archives

Recent Entries

• Hillary And The Diebold Effect

• Armed And Dangerous • the great subprime majority • Keeping honesty and principles in the closet? • Dousing a fire with the gasoline that started it? • Give me more atrocities! • Jeri Thompson Speaks • Coloreds Only • Starship • "Congrats, senator, you've just lost a supporter."

Links

Site Credits

|

|

And lets not forget the politicians who cajoled and threatened lenders into making loans to people who were bad credit risks.